Does Fitting a Dashcam Affect Your Car Insurance — and Can It Save You Money?

Fitting a dashcam can affect your car insurance positively. Some UK insurers offer discounts of 5–15% for dashcam users. More importantly, dashcam footage speeds up claims, deters fraud, and protects your no-claims bonus. You are not legally required to tell your insurer, but doing so is worth it.

A few years ago, I watched a driver in front of me slam his brakes for no reason. The car behind him — not me, thankfully — had no choice. It hit him. The driver ahead jumped out, phone already in hand, calling his insurer before the dust settled.

That was almost certainly a crash-for-cash attempt. And the driver behind? He had no dashcam. No evidence. He had to fight the claim for months.

That story is why I started looking seriously at dashcams — and why so many UK drivers now want to know whether fitting one actually changes anything with their insurance.

I’m Alex Rahman, and I’ve spent years researching car technology and motor insurance. The short answer is: yes, a dashcam can affect your insurance. But how it affects it depends on things most guides never explain.

By the end of this guide, you’ll know exactly what your insurer thinks about dashcams, how to use one to protect yourself, and whether it’s worth the money.

- Some UK insurers offer dashcam discounts of 5–15%, but you must ask — most won’t advertise it.

- Dashcam footage can resolve disputed claims faster and protect your no-claims bonus.

- You are not legally required to tell your insurer about a dashcam, but it can work in your favour.

- Footage can legally be used against you if it shows you were at fault — no hiding from it.

- A front-and-rear dashcam gives you stronger all-round protection than a front-only camera.

What Does a Dashcam Actually Do and Why Do Insurers Care?

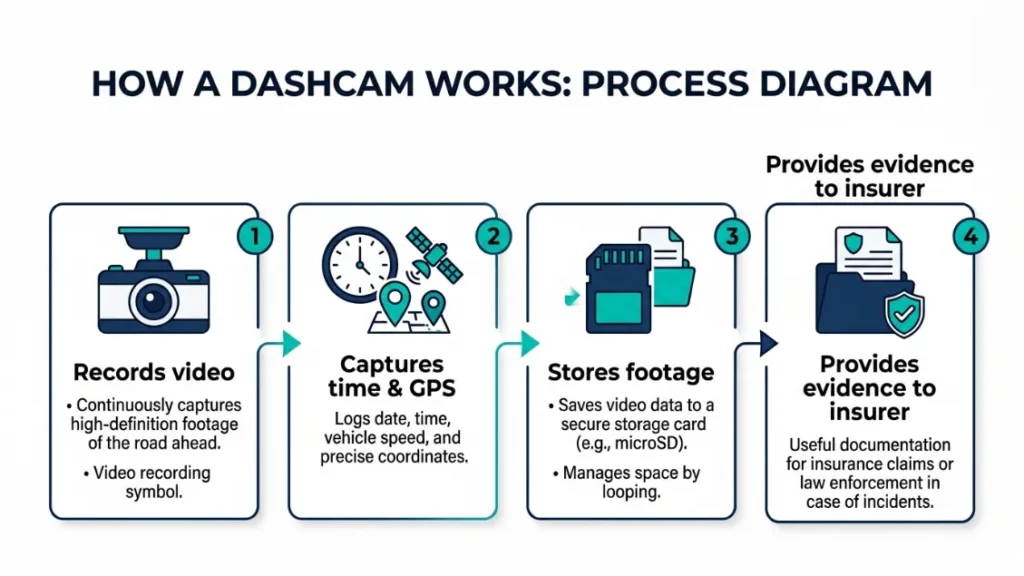

A dashcam is a small video camera that mounts to your windscreen and records the road continuously while you drive. It captures footage, timestamps, GPS location, and sometimes speed data. Insurers care because that footage removes guesswork from accidents and claims.

Before dashcams, disputed accidents came down to one driver’s word against another’s. That meant longer investigations, higher legal costs, and more fraudulent claims slipping through. A dashcam changes that dynamic entirely.

Insurers lose billions each year to fraudulent claims. According to the Association of British Insurers (ABI), fraud adds an estimated £50 to the average UK motor insurance premium. Dashcams cut into that number.

When a driver has clear video evidence, claims resolve faster. Fault gets established quickly. Legal disputes shrink. That saves the insurer money — and that saving can flow back to you as a driver.

How a Dashcam Records Evidence That Insurers Can Use

A dashcam records a continuous loop of video, overwriting old footage automatically unless an incident is detected. Most modern cameras from brands like Nextbase (the UK’s best-selling dashcam brand) use G-sensors to lock footage the moment an impact occurs. That locked clip stays saved even if the loop overwrites everything else.

The footage typically includes the date, time, GPS coordinates, and speed at impact. That data package is exactly what an insurer’s claims team needs to make a fast decision.

Always check that your dashcam saves footage to a reliable, Class 10 microSD card. Cheap cards corrupt under heat. Corrupted footage is no footage at all when you need it most.

Does a Dashcam Lower Your Car Insurance Premium in the UK?

A dashcam can lower your car insurance premium in the UK, but the discount is not guaranteed and not universal. Some insurers offer a direct reduction of 5–15% for drivers who fit and register a dashcam on their policy. Others count it as a positive risk signal without attaching a specific number to it.

The honest picture is this: the insurance market has not standardised dashcam discounts. Some insurers build the benefit into their overall risk assessment. Others offer it as a named add-on or loyalty feature.

What matters most is that you ask. Ring your insurer directly and ask whether they offer a dashcam discount or acknowledge dashcam use at renewal. Many do — they just don’t shout about it.

Which UK Insurers Offer a Dashcam Discount and How Much Is It?

Several major UK insurers acknowledge dashcam benefits, though the specifics change regularly. Direct Line, Aviva, and Admiral have all publicly commented on the positive role dashcams play in claim resolution. Some specialist insurers — particularly those targeting young or new drivers — actively encourage dashcam use alongside telematics policies.

In 2023, research by Nextbase found that over 60% of UK drivers believed a dashcam would benefit their insurance position. A separate survey by Compare the Market suggested that around 1 in 5 UK motorists had used dashcam footage to support an insurance claim.

The typical discount range is 5–15%, though some specialist young driver policies tied to dashcam-monitored schemes can go higher. For context, on a £900 annual premium, a 10% discount saves you £90 — more than the cost of most entry-level dashcams.

| Insurer | Dashcam Policy Stance | Potential Benefit |

|---|---|---|

| Direct Line | Acknowledges claim benefit | Faster claim resolution |

| Aviva | Positive risk signal | Potential premium reduction |

| Admiral | Claim evidence supporter | No-claims bonus protection |

| Specialist young driver insurers | Dashcam-monitored schemes | Up to 20%+ discount possible |

Why Most Insurers Won’t Advertise the Discount Upfront

Insurers price policies based on risk pools, not individual gadgets. If every driver claimed a dashcam discount without evidence, the system would collapse quickly. So most insurers treat dashcam ownership as a quiet positive — something that helps your case without being a headline offer.

Some also worry about liability. If they advertise dashcam discounts and then use footage against a claimant, they face reputational risk. So they keep it low-profile.

Your move: call your insurer before renewal. Mention you have a dashcam fitted and ask whether it affects your premium. It takes three minutes and can save real money.

How Does a Dashcam Help You Win an Insurance Claim?

A dashcam helps you win an insurance claim by providing timestamped, GPS-tagged video evidence of exactly what happened. This removes the he-said-she-said deadlock that delays most disputed claims and gives your insurer something concrete to work with immediately.

Without footage, a disputed claim can take months. With footage, many claims resolve in days. That speed matters because every extra week a claim sits open risks your no-claims bonus, your stress levels, and your time.

Your no-claims bonus (NCB) is often your most valuable insurance asset. Some drivers build up 5 years of NCB worth 60–70% off their premium. Losing it after a disputed accident you didn’t cause is genuinely expensive. A dashcam gives you the evidence to defend it.

What Happens If Dashcam Footage Shows You Were at Fault?

If dashcam footage clearly shows you were at fault, it will work against you in a claim. This is the part most dashcam guides avoid saying plainly — so I’ll say it clearly.

Your insurer can request your dashcam footage during a claim investigation. In some cases, the other party’s legal team can also request it through a court disclosure process. Deleting footage after an accident can be treated as evidence tampering.

Never delete dashcam footage after an accident. If a claim proceeds and the footage was erased, a court can draw negative inferences from that deletion. Keep all footage until any claim is fully closed.

The flip side: if you drive well, this is never a problem. Honest drivers with dashcams almost always benefit from footage. The camera rewards good driving and punishes careless driving — exactly as it should.

How Dashcams Stop Crash-for-Cash Fraud Targeting You

Crash-for-cash fraud happens when a criminal deliberately causes an accident to make a fraudulent insurance claim against an innocent driver. The ABI estimated in 2022 that staged accidents cost UK insurers over £340 million annually — a cost passed directly to every paying driver.

A dashcam is one of the most powerful deterrents against this crime. Fraudsters target drivers without cameras because there is no evidence to counter their false story. A visible dashcam on your windscreen signals to a potential fraudster that you have footage. Many simply move on to an easier target.

If you are targeted despite having a dashcam, the footage proves the staged nature of the accident. The braking pattern, speed differential, and road conditions all tell a clear story that no fraudster can argue against convincingly.

Crash-for-cash fraud is not rare. It happens on busy motorway slip roads, at roundabouts, and in car parks every day across the UK. A dashcam is not just a gadget — it is direct financial self-defence.

Do You Have to Tell Your Insurance Company You Have a Dashcam?

You are not legally required to tell your insurer that you have fitted a dashcam. A dashcam is a standard accessory, not a vehicle modification that changes the car’s mechanical specification. You do not need to declare it the way you would declare a new exhaust system or modified suspension.

However, telling your insurer can work in your favour for two reasons. First, it may trigger a discount or a positive note on your file. Second, if you submit dashcam footage as part of a claim, your insurer already knows the camera exists. That removes any question about why footage suddenly appeared.

Always tell your insurer if your dashcam is hardwired directly to the vehicle’s electrics. Hardwiring is a minor vehicle modification and, in the strictest reading of most policy terms, may need to be declared. Most insurers will not penalise you for it — but failing to mention it could give them grounds to complicate a future claim.

When you renew your policy, mention your dashcam to the insurer as a matter of routine. A single sentence — “I have a Nextbase 622GW fitted to my vehicle” — puts it on record and opens the door to a discount conversation.

Does Fitting a Dashcam Void Your Car Warranty or Damage Your Vehicle?

Fitting a dashcam does not void your car warranty if installed correctly. A suction-mount or adhesive dashcam attached to the windscreen is a removable accessory and has no impact on your manufacturer warranty whatsoever. The risk only arises with hardwired installations done badly.

If a hardwired dashcam is connected incorrectly to your vehicle’s fuse box — drawing too much power or creating an electrical fault — it can in theory cause issues that a manufacturer would dispute under warranty. A professional installation removes that risk entirely.

Hardwired vs. Plug-In Dashcam — Which Is Safer for Your Car?

A plug-in dashcam connects to your 12V socket or cigarette lighter port. It is safe, simple, and completely removable. It carries zero risk to your warranty or vehicle electrics. The trade-off is that it stops recording when you turn the engine off, so you lose parking mode protection.

A hardwired dashcam connects directly to the vehicle’s fuse box. It draws a low, constant trickle of power so the camera can monitor your parked car for knocks and break-in attempts. Brands like BlackVue and Viofo are well known for their hardwired parking mode systems.

- Choose a dashcam hardwiring kit rated for your car’s voltage (most are 12V/24V compatible).

- Identify the correct low-amperage fuse slot in your vehicle’s fuse box using the owner’s manual.

- Connect the hardwiring kit’s add-a-fuse adapter to a switched live fuse slot (one that turns off with the ignition) for normal use, or a permanent live for parking mode.

- Route the cable neatly along the A-pillar and headlining to keep it hidden and safe from airbag deployment zones.

- Set the low-voltage cut-off on the dashcam to at least 12V to prevent it draining your battery.

If you are not confident working with automotive electrics, a professional fitting centre will do this for £50–£80 in most UK cities. That cost buys you peace of mind and protects your warranty.

Dashcam vs. Telematics Black Box — Which One Saves More on Insurance?

A telematics black box typically saves more money on insurance than a dashcam alone, particularly for young or new drivers. A black box monitors your speed, acceleration, braking, and time of driving to build a risk profile. Insurers use that data to price your policy individually. Savings of 20–40% are common for safe young drivers on telematics policies.

A dashcam does not feed live data to your insurer. It records events passively and only becomes relevant when you share footage. So the direct premium impact is usually smaller.

| Feature | Dashcam | Telematics Black Box |

|---|---|---|

| Premium discount | 5–15% | 20–40% |

| Claim evidence | Strong (video) | Moderate (data only) |

| Privacy impact | Low (footage stays with you) | Higher (live data to insurer) |

| Fraud deterrence | High | Low |

| Best for | All drivers, especially experienced | Young or new drivers |

The good news: these two tools are not mutually exclusive. Some young driver insurers now offer telematics policies that also encourage dashcam use. Combining both gives you the maximum financial protection and the strongest claim evidence base.

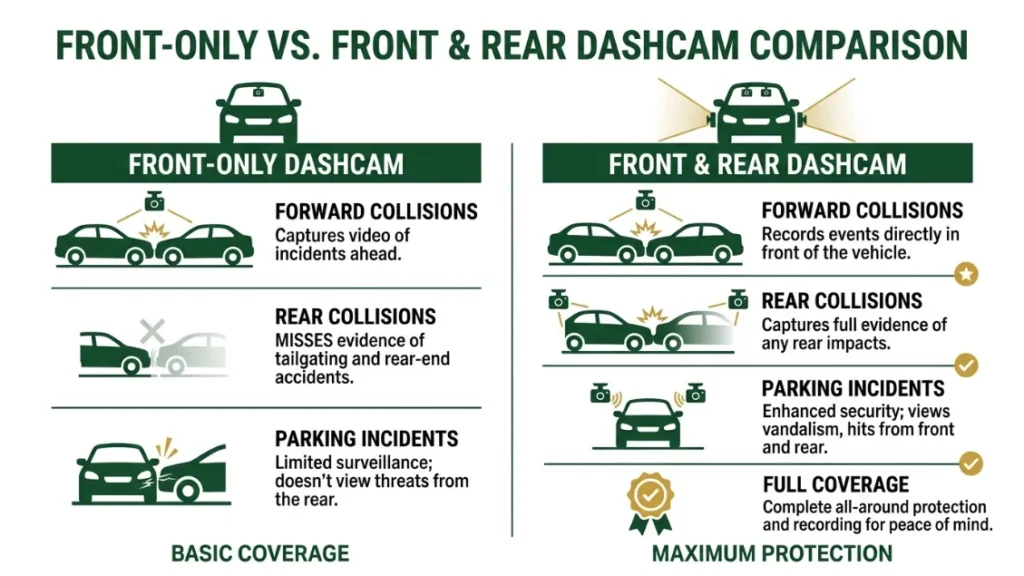

Front-Only vs. Front-and-Rear Dashcam — Which Protects Your Insurance More?

A front-and-rear dashcam provides stronger insurance protection than a front-only camera. The reason is simple: a large proportion of accidents involve the rear of your vehicle — rear-end collisions, car park scrapes, and hit-and-run incidents while parked. A front-only camera captures none of that.

Front-only cameras are excellent at recording what happens ahead of you. They catch brake-checking, red light violations, and at-fault drivers cutting across your lane. But if someone drives into the back of you and disputes fault, you have no footage.

For the best insurance protection, fit a dual-channel dashcam. Systems like the Nextbase 622GW with its rear camera module, or the Viofo A139 dual-channel kit, cover both angles and typically add only £30–£60 to the total cost. That is a small price for doubling your evidence coverage.

Front-only dashcams protect against forward collisions and fraud. Front-and-rear systems protect against rear collisions, parking incidents, and hit-and-run damage. If you want maximum insurance protection, choose a dual-channel system from day one.

Can Dashcam Footage Be Used Against You Legally?

Yes — dashcam footage can be used against you in both an insurance claim and a criminal investigation. If your footage shows you speeding, running a red light, using a phone, or driving carelessly at the time of an accident, that evidence is admissible and insurers and courts can act on it.

Police can also request dashcam footage as part of a road traffic investigation. In the UK, Operation Snap allows members of the public to submit dashcam footage of other drivers’ dangerous behaviour — and that same mechanism works in reverse.

This is not a reason to avoid fitting a dashcam. It is a reason to drive well. Honest, careful drivers have nothing to fear from their own footage. The camera is impartial — it records what happened, not what you wished had happened.

What GDPR Rules Say About Sharing Your Dashcam Footage

In the UK, dashcam footage captured for personal use — including for insurance claim purposes — falls under a domestic exemption from full GDPR compliance. You can record public roads and share that footage with your insurer or police without violating data protection law in most circumstances.

However, sharing footage publicly on social media — especially footage that identifies individuals or vehicle registration plates — enters a legal grey area. The Information Commissioner’s Office (ICO) advises caution around publishing footage that was not captured for journalistic or law enforcement purposes.

For a full breakdown of UK GDPR guidance on dashcam use, the ICO website is the authoritative source. The rule of thumb: share with your insurer freely, share with police freely, share on social media carefully.

How to Get the Most Out of Your Dashcam for Insurance Purposes

Getting the most from your dashcam for insurance means doing more than just plugging it in and forgetting it. A few simple habits turn a passive recording device into an active financial protection tool.

- Register your dashcam with your insurer at the next renewal and ask about a discount directly.

- Format your memory card every 4–6 weeks to prevent file corruption from continuous recording.

- Check that your G-sensor sensitivity is set to medium — too sensitive triggers on speed bumps; too low misses real impacts.

- After any incident, manually lock and back up the footage to a phone or laptop before it overwrites.

- Keep the lens clean — a smeared lens produces unusable footage when you need it most.

- If you submit footage to your insurer, send the original file — not a screen recording — to preserve metadata.

One more thing I always tell people: after a collision, stay calm and do not immediately show the other driver your dashcam footage. Wait until you have spoken to your insurer. Revealing your footage at the scene can change the dynamics of a claim before professionals have assessed it.

Store your dashcam footage in a cloud backup service. Some Nextbase and BlackVue models offer built-in cloud connectivity so footage uploads automatically to a secure server. If your camera is stolen or damaged in the accident, the footage still exists.

For a detailed overview of how dashcam evidence works in UK insurance disputes, the Association of British Insurers publishes accessible guidance on claims evidence standards.

Conclusion

Fitting a dashcam is one of the smartest moves a driver can make — not just for insurance discounts, but for complete on-road protection.

Yes, some UK insurers will reduce your premium. Yes, footage resolves claims faster and protects your no-claims bonus. Yes, a visible dashcam deters crash-for-cash fraudsters before an accident even happens. And yes, a front-and-rear dual system gives you far stronger coverage than a front-only camera.

The one truth most guides skip: a dashcam is impartial. It records what actually happened. If you drive carefully, that works entirely in your favour. If you don’t, it won’t. That honesty is what makes dashcam footage so powerful in the eyes of insurers and courts alike.

I’m Alex Rahman, and in my experience researching this space, no single car accessory under £100 delivers as much practical financial value as a well-fitted dashcam. Talk to your insurer, fit the camera properly, and drive with confidence.

Frequently Asked Questions

Does having a dashcam reduce car insurance in the UK?

Some UK insurers offer a discount of 5–15% for drivers who fit a dashcam and declare it. Not all insurers advertise this openly, so it is worth asking directly at renewal. The biggest financial benefit is usually the protection of your no-claims bonus through faster claim resolution.

Do I have to tell my insurer I have a dashcam?

You are not legally required to declare a standard plug-in dashcam. However, if your dashcam is hardwired to the vehicle’s electrics, it is worth mentioning to your insurer as a minor modification. Declaring it also opens the door to a discount and avoids any ambiguity if you later submit footage for a claim.

Can dashcam footage be used against me in a claim?

Yes. If dashcam footage shows you were at fault — speeding, failing to stop, or driving carelessly — insurers and courts can use it against you. Never delete footage after an accident, as this can be treated as evidence tampering. Honest drivers with good habits have nothing to fear from their own footage.

Does fitting a dashcam void my car warranty?

A suction-mount or adhesive dashcam does not void your car warranty under any normal circumstances. A hardwired dashcam fitted by a professional also carries negligible risk. The only genuine warranty risk comes from amateur hardwiring that causes electrical faults — so get it done professionally if you are unsure.

Which is better for saving on insurance — a dashcam or a black box?

A telematics black box typically delivers larger premium reductions of 20–40%, particularly for young or new drivers, by monitoring driving behaviour in real time. A dashcam saves less directly on premium but provides stronger claim evidence and fraud deterrence. Many drivers benefit from using both together.

Does a front-and-rear dashcam make a difference for insurance claims?

Yes — significantly. A front-and-rear dual-channel dashcam records rear-end collisions, parking incidents, and hit-and-run damage that a front-only camera completely misses. For comprehensive insurance protection, a dual-channel system gives you far stronger evidence coverage for the same basic principle of continuous recording.

I’m Alex Rahman, a car enthusiast and automotive writer focused on practical solutions, car tools, and real-world driving advice. I share simple and honest content to help everyday drivers make better decisions.