How Much Does a Dashcam Decrease Insurance?

A dashcam can reduce your car insurance premium by 5% to 15% with insurers that formally recognise them. Most savings come indirectly — through faster claim resolution and fraud prevention — rather than a guaranteed upfront discount. Not every insurer offers one, so always ask at renewal.

How Much Does a Dashcam Decrease Insurance — and Is the Saving Worth It?

A few years ago, a driver in Birmingham cut in front of me at a roundabout and then claimed I hit him. No witnesses. His word against mine. I had no footage and ended up paying an excess I still resent.

That experience sent me straight to buy a dashcam. And it made me wonder — could this small camera actually save me money beyond just protecting me legally?

I’m Alex Rahman, and I’ve spent years researching how dashcams interact with car insurance policies across the UK and US. The answer is more nuanced than most people expect. Some drivers save real money. Others see zero discount but still benefit massively at claim time.

Here is everything you need to know — including the exact steps to maximize whatever saving is available to you.

- Dashcams can cut premiums by 5% to 15% with insurers that formally offer the discount.

- Many insurers don’t advertise a dashcam discount — but footage still reduces claim costs, which protects your no-claims bonus.

- Front-plus-rear camera setups provide stronger protection than front-only systems.

- You must proactively tell your insurer you have a dashcam — it rarely happens automatically.

- A dashcam costing £50 to £150 typically pays for itself within one or two renewal cycles if you get the discount.

What Discount Does a Dashcam Actually Get You on Car Insurance?

A dashcam discount typically ranges from 5% to 15% off your annual car insurance premium, depending on your insurer and location — though many providers offer no formal discount at all, even if footage helps you enormously during a claim.

This is the number most people search for, and the honest answer is: it varies a lot. There is no industry-standard dashcam discount. Insurance is risk-based, and each company prices that risk differently.

What is consistent is this: insurers that do offer a dashcam discount do so because footage reduces their own costs — fewer fraudulent payouts, faster fault decisions, and lower litigation expenses. They pass some of that saving on to you.

Why the Exact Number Varies by Insurer and Country

In the UK, Admiral Insurance has publicly acknowledged dashcam footage as a factor in claim outcomes, and some specialist providers offer structured discounts between 10% and 12.5%. In the US, the discount culture is different — most insurers integrate dashcam-style benefits through telematics programs like Progressive’s Snapshot rather than a flat dashcam rate reduction.

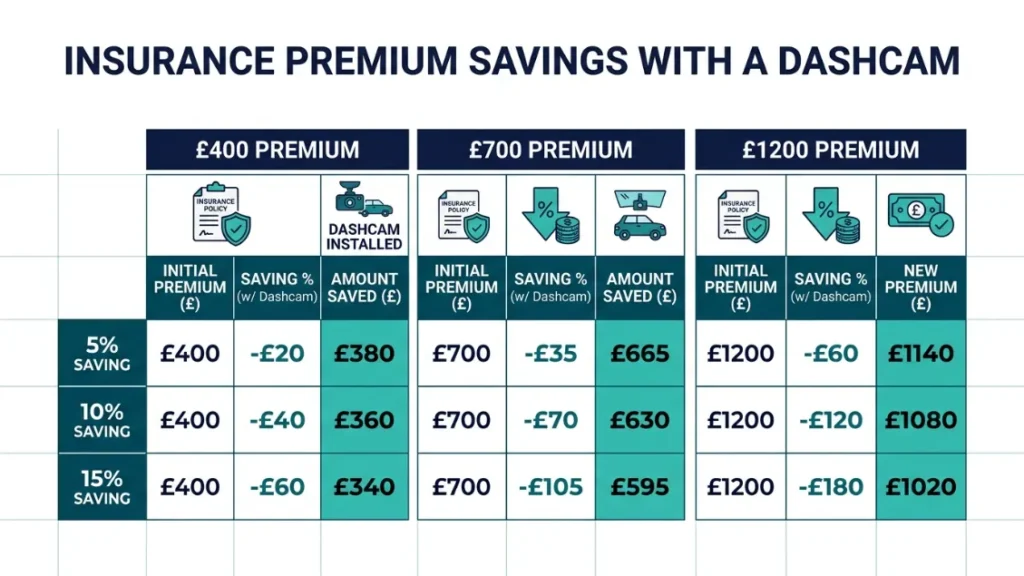

Your premium also depends on your age, vehicle, postcode or zip code, and claims history. A 10% dashcam discount on a £400 annual premium saves you £40. On a £1,200 premium for a young driver, that same 10% saves £120 — which covers the cost of a solid mid-range dashcam in one year.

What the Average Saving Looks Like in Real Money

| Annual Premium | 5% Discount | 10% Discount | 15% Discount |

|---|---|---|---|

| £400 | £20/year | £40/year | £60/year |

| £700 | £35/year | £70/year | £105/year |

| £1,200 | £60/year | £120/year | £180/year |

Always ring your insurer directly and ask: “Do you offer a discount for drivers who use a dashcam?” Many agents won’t volunteer this information unless you ask first.

Why Do Insurance Companies Care Whether You Have a Dashcam?

Insurers care about dashcams because footage directly reduces two of their biggest costs: fraudulent claims and drawn-out fault disputes. When a claim resolves quickly and clearly, the insurer spends less — and a portion of that saving can flow back to you as a lower premium.

This is not about rewarding good drivers for safety. It is pure risk mathematics. Insurers price premiums based on expected payout cost. Anything that reduces that cost is worth a discount.

How Dashcam Footage Stops Fraudulent Claims Before They Cost Everyone

“Crash for cash” fraud — where criminals deliberately cause accidents to claim insurance money — costs the UK insurance industry an estimated £340 million every year, according to the Association of British Insurers. That cost gets spread across every premium in the country.

A dashcam recording a deliberate brake-check or a staged sideswipe gives the insurer irrefutable evidence to reject a fraudulent claim. With footage, the fraudster moves on — your insurer saves tens of thousands of pounds, and the claim never touches your no-claims bonus.

The Insurance Fraud Bureau (IFB) reports that dashcam footage has directly helped defeat dozens of organized fraud rings in the UK. Each defeat removes a cost from the system that would otherwise raise prices for everyone.

How Footage Speeds Up Fault Decisions and Lowers Claim Costs

Fault determination — figuring out who caused the accident — is the most expensive part of most claims. Legal fees, loss adjusters, and medical assessments all pile up when two drivers disagree. Clear video footage can collapse a months-long dispute into a single phone call.

Insurers know this. Fewer hours of investigation means lower costs. That efficiency is part of why dashcam-friendly insurers can offer a discount without losing money.

When footage settles fault in seconds instead of months, the legal and administrative cost of a claim can drop by 40% to 60%. That saving is exactly what funds your dashcam discount.

Which Insurance Companies Offer a Dashcam Discount Right Now?

Not every insurer advertises a formal dashcam discount, but several UK providers and US programs actively reward or benefit dashcam users — either through reduced premiums or claim-handling advantages that protect your bonus.

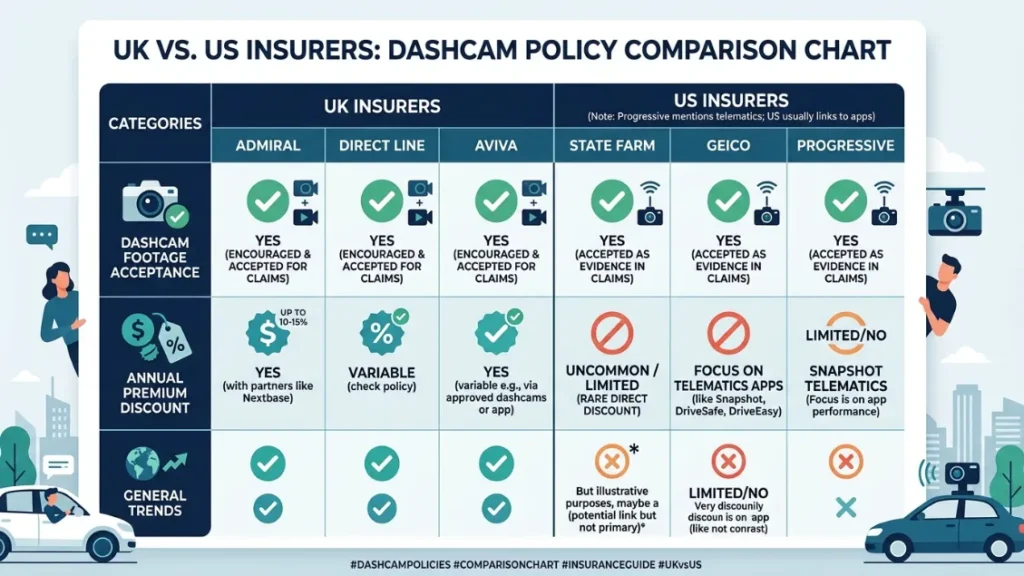

UK Insurers That Reward Dashcam Drivers

In the UK, the dashcam discount landscape has grown significantly since 2018. Several providers now factor dashcam use into their pricing or claims process:

- Admiral Insurance — accepts dashcam footage in claims and considers it during fault assessment.

- Nextbase Insurance — a dedicated dashcam-linked policy that uses Nextbase camera data as a primary claims tool, with discounts built into the model.

- Direct Line — accepts customer-submitted dashcam footage during the claims process, which can accelerate resolution and protect your no-claims bonus.

- Aviva — allows dashcam footage as supporting evidence, which can influence liability decisions in borderline cases.

- Specialist brokers — several UK insurance brokers (particularly those targeting young or high-risk drivers) offer explicit dashcam discounts of 10% to 12.5%.

Insurer policies change frequently. Always confirm current dashcam discount availability directly with your provider before renewal — what was true in 2022 may no longer apply today.

US Insurers and the Telematics Alternative

In the United States, dedicated dashcam discounts are rare at the major insurer level. Most large carriers — including State Farm, Geico, and Allstate — do not offer a formal dashcam premium reduction as of 2024.

Instead, US drivers get equivalent benefits through telematics programs. These use a plug-in device or smartphone app to monitor your driving behavior. Progressive’s Snapshot program, for example, advertises savings of up to 30% for safe drivers. Liberty Mutual’s RightTrack and Nationwide’s SmartRide work similarly.

Some US insurers — particularly smaller regional carriers — do accept dashcam footage in claims disputes, which protects your no-claims history even without a formal discount. Check with your specific carrier using the Insurance Information Institute’s insurer checklist as a starting point.

Does a Dashcam Help You After an Accident — Even Without a Discount?

Yes — and for many drivers, this indirect benefit is worth more than any premium discount. Dashcam footage can protect your no-claims bonus, prove your innocence in a disputed claim, and prevent a fraudulent claim from ever reaching your insurer in the first place.

The no-claims bonus is one of the most valuable things a driver builds over time. In the UK, five years of no-claims can reduce a premium by 60% to 75%. Losing it in one disputed accident — an accident you didn’t cause — costs far more than any dashcam ever will.

How Footage Protects You When the Other Driver Lies

Sound familiar? The other driver says you pulled out in front of them. There are no witnesses. The insurer splits liability 50/50 and both premiums go up. This is one of the most common and frustrating outcomes in minor accidents.

A dashcam recording of the same moment ends that dispute instantly. Your footage shows exactly what happened. The other driver’s account collapses. Your no-claims bonus stays intact. That protection is worth hundreds or even thousands of pounds over a driving lifetime.

Nextbase (the UK’s best-selling dashcam brand with over 3 million units sold) designs cameras specifically with insurance evidence in mind — their 622GW model records in 4K resolution with GPS speed logging, which timestamps and geotags every frame for maximum evidential value.

Can Dashcam Footage Ever Work Against You?

Yes, it can — and this is something most dashcam guides skip. If your dashcam captures you driving carelessly, speeding, or using your phone, that footage could be requested by an insurer or used against you in court.

In the UK, insurers can request dashcam footage as part of a claim investigation. If you caused an accident and your footage proves it, you cannot hide behind ambiguity. The flip side: if you were driving correctly, that same footage completely vindicates you.

A dashcam rewards safe drivers and penalises careless ones. If you drive well, it is your best ally. Use it as a daily reminder to drive the way you’d want to be seen on camera.

How Do You Actually Get the Insurance Discount for Your Dashcam?

Getting a dashcam insurance discount requires you to take action — it never happens automatically. You must contact your insurer, confirm they offer the discount, and provide proof that your dashcam is installed and operational.

Most drivers with dashcams are not getting any discount simply because they never told their insurer. The camera sits on the windscreen, the insurer has no idea it exists, and the saving never materialises.

Steps to Notify Your Insurer and Maximize Your Saving

- Buy a dashcam from a recognised brand — Nextbase, Garmin, or Vantrue are insurer-familiar names.

- Install it correctly on your windscreen within the legal wipe area — poor placement can invalidate the benefit.

- Note your dashcam model, serial number, and installation date.

- Call your insurer (or use their online portal) and ask directly: “Do you offer a discount for dashcam users?”

- Submit proof of purchase and any required documentation they request.

- If your current insurer offers nothing, get quotes from dashcam-friendly providers at renewal — use this as a negotiating point.

- Test your dashcam’s footage quality regularly to ensure it captures clear, timestamped video.

Is a Dashcam Worth Buying Just to Lower Your Insurance Cost?

For most drivers, a dashcam is worth buying — but not for the insurance discount alone. The real value is in the protection it provides at claim time, which safeguards a no-claims bonus worth far more than any annual premium reduction.

Let me give you the honest breakdown. A decent dashcam costs £50 to £200. A 10% discount on a £600 premium saves you £60 per year. In year one, you roughly break even. From year two onward, the saving is pure profit — plus you have footage protection every single day.

Dashcam vs. Telematics — Which Saves You More?

| Factor | Dashcam | Telematics / Black Box |

|---|---|---|

| Typical saving | 5% – 15% | 10% – 40% |

| Monitors driving behaviour | No (footage only) | Yes (speed, braking, time) |

| Protects in disputed claims | Strong — visual proof | Moderate — data only |

| Privacy impact | Low — you control footage | High — insurer sees all data |

| Best for | Experienced drivers | New or young drivers |

| Upfront cost | £50 – £200 once | Often free (device) |

The Real Return on Investment for a Dashcam

One protected no-claims bonus is worth more than years of small discounts. In the UK, losing five years of no-claims after a disputed accident you didn’t cause can cost an extra £300 to £600 per year for three or more years. That is a potential loss of £1,800 or more — erased entirely by one clear piece of footage.

A dashcam’s ROI comes from two sources: the annual premium discount (5% – 15% if your insurer offers it) and the protection of your no-claims bonus. The second benefit is typically worth far more over a 5-year driving period than the discount alone.

What Type of Dashcam Gives You the Best Insurance Benefit?

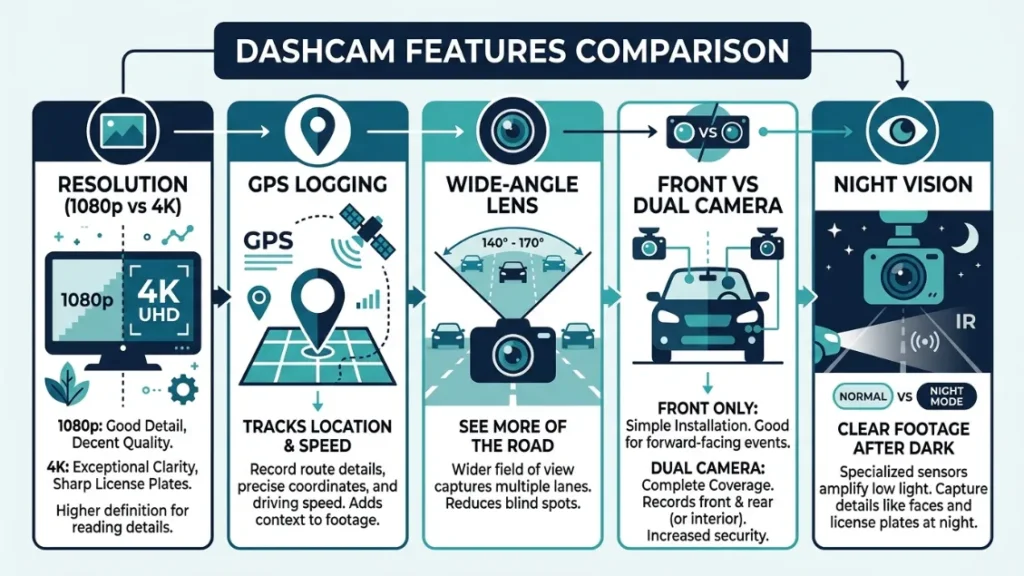

For insurance purposes, the best dashcam records clear 1080p or higher footage with GPS logging, a wide field of view, and a reliable loop-recording system — with a rear camera adding significant protection in rear-collision disputes.

Not all dashcams are equal in evidential value. A blurry 720p recording with no timestamp gives an insurer far less to work with than a crisp 4K GPS-tagged video that proves your speed and location frame by frame.

Front-Only vs. Front and Rear — Which Do Insurers Prefer?

Rear-end collisions are among the most disputed accident types. The rear driver almost always claims the front driver braked suddenly. A rear-facing camera proves or disproves this claim instantly.

UK insurer data consistently shows that dual-channel (front and rear) dashcam setups resolve rear-impact claims faster than front-only systems. If your insurer offers a structured dashcam discount, some now require or prefer a dual-channel setup to qualify at the higher tier.

Features That Matter Most for Insurance Purposes

- Resolution: 1080p minimum; 1440p or 4K preferred for reading number plates.

- GPS logging: Timestamps your speed and location — critical for disputed speeding allegations.

- Wide-angle lens: 140° to 170° captures adjacent lanes and reduces blind spots in footage.

- Loop recording: Overwrites old footage automatically so storage never fills up during normal driving.

- G-sensor / incident lock: Automatically saves and protects footage when it detects a collision — prevents accidental overwrite of the moment that matters most.

- Night vision / HDR: Clear footage in low light is essential — most accidents happen in dawn, dusk, or wet conditions.

- Cloud backup: Premium feature on models like the Nextbase 622GW that protects footage even if the camera is stolen or damaged in the accident.

Always check that your dashcam is positioned within the legal windscreen zone — in the UK, this means behind the rear-view mirror and within the swept area of the wipers. An incorrectly placed camera could create a legal complication if footage is ever challenged in court.

For more on what makes dashcam footage legally useful, the UK Government driving regulations page outlines relevant windscreen and distraction rules you should know.

Conclusion

A dashcam can reduce your car insurance premium by 5% to 15% — but only if your insurer formally recognises it and you take the step of telling them. Many drivers miss that saving entirely because the camera sits on the windscreen and the conversation never happens.

More importantly, the indirect protection a dashcam provides — the no-claims bonus you never lose, the fraudulent claim that gets rejected, the disputed accident that resolves in your favour — is worth far more than any annual discount.

My advice, after years of research and one very expensive lesson at a roundabout in Birmingham: buy the dashcam, choose a model with GPS and a rear camera, tell your insurer, and drive knowing every journey is documented. It is one of the most cost-effective investments a driver can make.

— Alex Rahman

Frequently Asked Questions

Does having a dashcam automatically lower your insurance premium?

No — a dashcam does not automatically reduce your premium. You must contact your insurer directly, confirm they offer a dashcam discount, and provide proof of installation. Many insurers won’t apply any reduction unless you proactively ask.

How much does a dashcam save on car insurance per year?

Drivers with insurers that formally recognise dashcams typically save between 5% and 15% on their annual premium. On a £700 policy, that equals £35 to £105 per year. Savings vary significantly by provider, age, and location.

Which UK insurers give a discount for dashcam drivers?

Nextbase Insurance and several specialist UK brokers offer structured dashcam discounts of up to 12.5%. Admiral, Direct Line, and Aviva accept dashcam footage in claims, which protects your no-claims bonus even if they don’t advertise a formal discount percentage.

Can dashcam footage be used against you in an insurance claim?

Yes. If your footage captures you speeding, using a phone, or driving carelessly, an insurer or court can request and use that evidence against you. Dashcams reward safe drivers — they make it impossible to hide fault if you genuinely caused the accident.

Is a dashcam worth it if my insurer offers no discount?

Yes. The primary financial value of a dashcam is protecting your no-claims bonus. Losing five years of no-claims in a disputed accident can cost £1,500 to £2,000 in higher premiums over three years — a loss that one clear piece of footage could prevent entirely.

What is the best dashcam to get for insurance purposes?

For insurance purposes, choose a dashcam with at least 1080p resolution, GPS logging, a G-sensor incident lock, and a rear camera. Brands like Nextbase, Garmin, and Vantrue all produce models between £80 and £200 that meet these criteria reliably.

{

“@context”: “https://schema.org”,

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “Does having a dashcam automatically lower your insurance premium?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “No — a dashcam does not automatically reduce your premium. You must contact your insurer directly, confirm they offer a dashcam discount, and provide proof of installation. Many insurers won’t apply any reduction unless you proactively ask.”

}

},

{

“@type”: “Question”,

“name”: “How much does a dashcam save on car insurance per year?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Drivers with insurers that formally recognise dashcams typically save between 5% and 15% on their annual premium. On a £700 policy, that equals £35 to £105 per year. Savings vary significantly by provider, age, and location.”

}

},

{

“@type”: “Question”,

“name”: “Which UK insurers give a discount for dashcam drivers?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Nextbase Insurance and several specialist UK brokers offer structured dashcam discounts of up to 12.5%. Admiral, Direct Line, and Aviva accept dashcam footage in claims, which protects your no-claims bonus even if they don’t advertise a formal discount percentage.”

}

},

{

“@type”: “Question”,

“name”: “Can dashcam footage be used against you in an insurance claim?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes. If your footage captures you speeding, using a phone, or driving carelessly, an insurer or court can request and use that evidence against you. Dashcams reward safe drivers — they make it impossible to hide fault if you genuinely caused the accident.”

}

},

{

“@type”: “Question”,

“name”: “Is a dashcam worth it if my insurer offers no discount?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes. The primary financial value of a dashcam is protecting your no-claims bonus. Losing five years of no-claims in a disputed accident can cost £1,500 to £2,000 in higher premiums over three years — a loss that one clear piece of footage could prevent entirely.”

}

},

{

“@type”: “Question”,

“name”: “What is the best dashcam to get for insurance purposes?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “For insurance purposes, choose a dashcam with at least 1080p resolution, GPS logging, a G-sensor incident lock, and a rear camera. Brands like Nextbase, Garmin, and Vantrue all produce models between £80 and £200 that meet these criteria reliably.”

}

}

]

}

I’m Alex Rahman, a car enthusiast and automotive writer focused on practical solutions, car tools, and real-world driving advice. I share simple and honest content to help everyday drivers make better decisions.