How Much Does a Dash Cam Reduce Insurance?

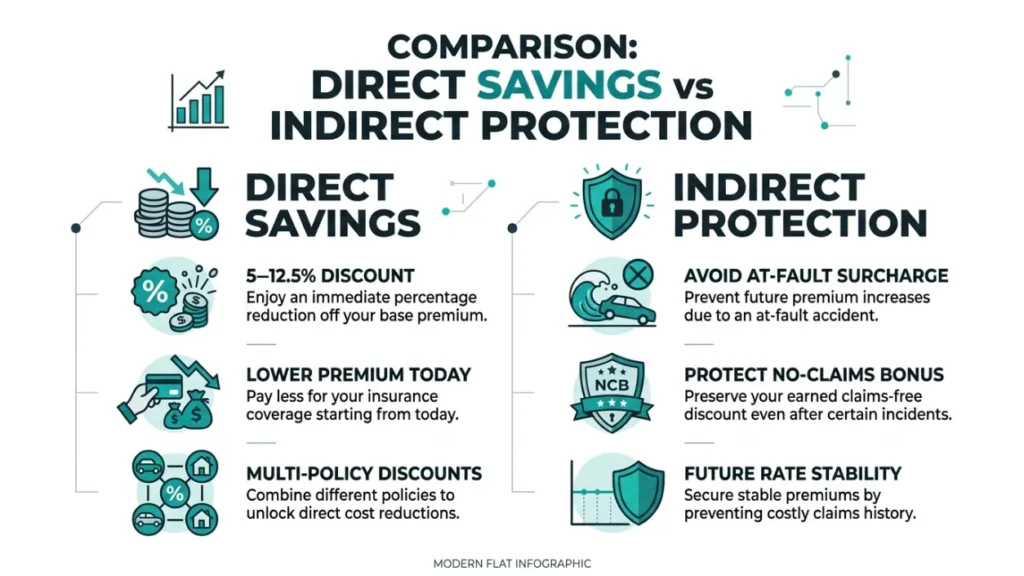

A dash cam can reduce car insurance by 5–20% with select insurers that offer explicit discounts. Even where no discount exists, a dash cam protects your no-claims bonus and shields you from at-fault surcharges — indirect savings that often exceed $200–$500 per year.

A few years ago, a friend of mine got rear-ended at a red light. The other driver claimed my friend reversed into him. No witnesses. No camera. My friend’s insurer sided with the other driver, and his premium jumped $340 the following year.

He bought a dash cam the next week.

I’m Alex Rahman, and I’ve spent years researching how technology affects personal finance — including car ownership costs. The question I hear most is simple: does a dash cam actually lower your insurance?

The honest answer has two parts. Yes, some insurers give a direct discount. But the bigger savings are hiding somewhere most people don’t look. Let’s break it all down.

- Some UK insurers offer direct dash cam discounts of 5–12.5%, but most US insurers do not yet have formal programs.

- The biggest financial benefit is indirect — avoiding a single at-fault label can save hundreds of dollars annually for years.

- Dash cam footage protects you from crash-for-cash scams, a fraud category that cost UK insurers over £340 million in 2022.

- For insurance use, your dash cam needs GPS, a timestamp, and at least 1080p resolution to be taken seriously.

- A quality dash cam pays for itself within months when you factor in full financial protection — not just headline discounts.

What Exactly Can a Dash Cam Do for Your Insurance?

A dash cam offers two types of insurance benefit: a direct premium discount from your insurer, and indirect financial protection that prevents your premium from rising after an accident. Most people only know about the first type — and that’s where they underestimate the real value.

Think of it like this. A discount saves you money today. Indirect protection saves you money for the next three to five years — every year — after an incident you didn’t cause.

The Direct Discount — What Insurers Actually Offer

Direct dash cam discounts exist, but they are not universal. Select insurers — mainly in the UK — reward drivers for fitting a qualifying dash cam by reducing their annual premium. The typical range runs from 5% to 12.5%, though exact figures depend on your insurer, your driving record, and the cam model you use.

Admiral Insurance, one of the UK’s largest car insurers, has publicly acknowledged dash cams as a factor in lower risk pricing. Insurers like Swiftcover and certain brokers through comparison sites also factor dash cam ownership into quotes.

The logic is straightforward. A driver with a dash cam is statistically more careful. They know they’re being recorded. And if an accident happens, the footage cuts claims investigation time and reduces fraudulent payouts — both of which lower insurer costs.

Always tell your insurer you have a dash cam — even if they don’t advertise a discount. Some insurers apply savings quietly, and others will note it on your file, which helps during a claim dispute.

The Indirect Savings That Matter Even More

Here is the part of the story most articles skip. Even if your insurer gives zero discount for owning a dash cam, the camera still protects you from one of the most expensive events in car ownership: being wrongly labeled at fault for an accident.

In the US, a single at-fault accident surcharge raises your premium by an average of 42–49%, according to data from the Insurance Information Institute. On a $1,500 annual policy, that’s a $630 increase — per year — often lasting three to five years.

A dash cam that costs $100 to $250 could prevent a cost of $1,800 to $3,150 over three years. That is not a discount. That is financial armor.

Which Insurance Companies Offer Dash Cam Discounts in the UK?

UK insurers are ahead of most markets when it comes to recognizing dash cams formally. Several companies either offer direct discounts or factor dash cam ownership into their risk pricing models.

| Insurer | Dash Cam Policy | Estimated Benefit |

|---|---|---|

| Admiral | Accepts footage in claims; pricing considers cam ownership | Varies by policy |

| Swiftcover | Dash cam discount program | Up to 12.5% |

| Hastings Direct | Accepts dash cam footage; no stated blanket discount | Claim protection value |

| Direct Line | Accepts footage as claim evidence | Claim protection value |

| Various brokers | Comparison site quotes may factor cam ownership | 5–10% depending on profile |

Important: Policies change frequently. Always confirm directly with your insurer whether a dash cam discount applies to your specific policy and which cam models qualify.

UK brand Nextbase — trusted by over two million drivers — has partnered with several insurers directly. Their Nextbase Insurance portal connects your cam to insurers who specifically recognize Nextbase footage in claims. This is the closest thing to a guaranteed discount program the UK market currently offers.

Do US Insurance Companies Give Discounts for Dash Cams?

In the United States, formal dash cam discount programs are rare. Most major US insurers — including State Farm, GEICO, Allstate, and Progressive — do not currently advertise a structured dash cam discount on personal auto policies as of 2024. This does not mean a dash cam is worthless in the US market. It means the benefit works differently.

US insurers focus more on telematics programs — devices or apps that monitor acceleration, braking, and mileage. Progressive Snapshot, State Farm Drive Safe & Save, and Allstate Drivewise are examples. These programs can save 10–30% for safe drivers. A dash cam complements these programs but does not replace them in the US context.

Where a US dash cam earns its value is in claims. The Insurance Information Institute reports that disputed liability claims are one of the costliest claim types for both insurers and drivers. Footage that clearly establishes fault speeds resolution and prevents wrongful at-fault designation — protecting your multi-year premium rate.

Do not assume your US insurer will automatically accept dash cam footage. Call them before an accident occurs. Ask specifically: “Will you accept dash cam footage as evidence in a liability dispute?” Get the answer in writing or by email.

How Does a Dash Cam Save You Money Even Without a Discount?

A dash cam’s biggest financial contribution is not the discount — it is the protection it provides against costs you would otherwise absorb silently for years. Two mechanisms drive this: no-claims bonus protection and defense against staged accident fraud.

Protecting Your No-Claims Bonus After an Accident

Your no-claims bonus (NCB) or no-claims discount (NCD) is one of the most valuable assets on your car insurance policy. In the UK, a five-year no-claims bonus can reduce your premium by 50–65%. Losing it — even partially — after one disputed accident is a serious financial blow.

When an accident is disputed and no clear evidence exists, insurers often split liability or label both parties at fault. Dash cam footage changes that. A clear recording proves who caused the incident, preserving your NCB and keeping your long-term premium low.

In the US, an at-fault accident stays on your record for three to five years. That premium surcharge compounds annually. One piece of footage that clears your name is worth years of savings.

Stopping Crash-for-Cash Scams Before They Cost You

Crash-for-cash fraud is exactly what it sounds like. A criminal deliberately causes or stages an accident — often a sudden brake on a motorway — then claims the innocent driver behind them caused the collision. The Insurance Fraud Bureau (IFB) estimated this type of fraud costs UK insurers over £340 million annually, adding roughly £50 to the average UK motor premium each year.

Dash cam owners are rarely targeted by crash-for-cash scammers. The camera is visible from outside the car. Fraudsters move on to easier targets. This deterrence effect alone has measurable value.

And if a scammer does target you? The footage is your complete defense.

The deterrence effect is real. Research from the IFB found that crash-for-cash hotspots shifted away from motorways where dash cam adoption increased. Criminals pick targets who can’t fight back — a visible dash cam makes you the wrong target.

How Much Could You Actually Save? A Real-World Numbers Breakdown

Let’s put real numbers on this. Here is a side-by-side comparison of a driver with and without a dash cam, covering both direct discounts and indirect protection over three years.

| Scenario | Without Dash Cam | With Dash Cam |

|---|---|---|

| Annual premium (base) | $1,500 | $1,425 (5% discount) |

| After disputed accident (at-fault surcharge ~42%) | $2,130/year | $1,425/year (footage clears fault) |

| 3-year total premium cost | $5,890 | $4,275 |

| Dash cam cost (one-time) | $0 | $150 |

| 3-Year Net Saving | — | $1,465 |

This scenario assumes one disputed accident over three years — which is not uncommon for most drivers. The dash cam pays for itself within the first month of avoiding a single surcharge.

Direct discount: 5–12.5% with qualifying UK insurers. Indirect savings: up to $1,500+ over three years by avoiding at-fault surcharges and protecting no-claims bonuses. Total financial case for a $100–$250 dash cam is strong regardless of whether your insurer offers a formal discount.

What Happens When You Use Dash Cam Footage in an Insurance Claim?

Submitting dash cam footage to your insurer is straightforward, but doing it correctly matters. Footage that is poorly stored, low resolution, or missing a timestamp may be dismissed or questioned. Here is exactly how the process works and how to give your footage the best chance of being accepted.

Step-by-Step: How to Submit Dash Cam Evidence to Your Insurer

- Stop loop recording immediately. Most dash cams overwrite old footage. Protect the clip by locking it via the cam’s emergency button or removing the SD card.

- Copy the file to a safe location. Save to your phone, laptop, or cloud storage as soon as possible. Create two backup copies.

- Note the exact timestamp. Write down the date, time, and GPS location shown in the footage before you do anything else.

- Contact your insurer within 24 hours. Report the incident and specifically state you have dash cam footage available.

- Follow your insurer’s preferred format. Some accept email attachments. Others use a portal or require a physical SD card copy. Ask first.

- Do not edit or crop the footage. Submit the complete, unedited clip. Edited footage loses credibility and may be rejected entirely.

- Keep the original SD card untouched. Store it safely. If the claim goes to dispute or court, the original file is your legal evidence.

Most insurers resolve claims faster when footage is available. Admiral has publicly stated that dash cam evidence speeds up their claims process significantly. Faster resolution means less time in a courtesy car and a quicker return to normal — another indirect financial benefit.

What Dash Cam Features Do You Actually Need for Insurance Benefits?

Not every dash cam delivers equal insurance value. A cheap, no-name camera with blurry footage and no timestamp is worse than useless in a claim — it adds cost without protection. Here are the features that genuinely matter for insurance purposes.

- Minimum 1080p Full HD resolution: Required to capture license plates clearly at speed. 1440p or 4K is better. Anything below 1080p is insufficient for claim evidence.

- GPS tracking: Records your speed, location, and route. Essential for speeding disputes and proving you were at the location stated.

- Accurate timestamp: Date and time must be embedded in the footage. Without it, the footage timeline can be challenged.

- Wide-angle lens (at least 140°): Captures events in adjacent lanes, not just directly ahead. Side-swipe incidents require wider coverage.

- Dual-channel (front and rear): Rear-end collisions are the most common accident type. Rear cam footage is frequently decisive in dispute resolution.

- Parking mode: Records incidents while your car is unattended. Covers hit-and-run in parking lots — a common claim type that is otherwise impossible to prove.

- Loop recording with locked files: Ensures continuous recording without SD card management, while allowing specific clips to be protected from overwrite.

Nextbase’s 522GW (UK) and Vantrue’s N4 Pro (US) both include GPS, 1440p resolution, dual-channel capability, and parking mode — meeting every insurance-relevant benchmark at a mid-range price point.

If you drive in the UK, check whether your dash cam appears on your insurer’s approved list before you buy. Some UK insurers only recognize specific brands or models in their discount programs. A quick phone call before purchase can save you from buying the wrong cam.

Can a Dash Cam Ever Work Against You in a Claim?

Yes — and this is the honest part most articles leave out. A dash cam records everything, including your own mistakes. If you ran a red light, followed too closely, or were distracted before an accident, that footage will show it. Your insurer may use it to determine your own liability.

This is not a reason to avoid a dash cam. It is a reason to drive consistently well — which is the behavior insurers want to reward anyway. If you drive safely, the camera protects you. If you make errors, the camera records reality — and reality was going to come out in a claim investigation regardless.

There is also a privacy consideration in some markets. In Germany, for example, continuous dash cam recording in public spaces has faced legal scrutiny under privacy law. If you drive across European borders regularly, check the local regulations for each country before using a cam.

Never delete or selectively hide footage after an accident. Destroying evidence in an insurance claim or legal proceeding is a serious offense that can void your policy and expose you to fraud allegations. Always submit complete, unedited footage.

Is a Dash Cam Worth It? The Honest ROI Verdict

A quality dash cam costs between $80 and $300. It lasts four to six years with proper care. Over that period, the financial case is clear for almost every driver.

If your insurer offers a direct discount of 5–12.5%, you recover the camera cost within one to two policy years. If your insurer offers no discount, one avoided at-fault surcharge — worth hundreds of dollars annually for three or more years — makes the purchase obvious.

The drivers who benefit most are those who commute daily, drive on busy motorways, or live in areas with high accident frequency. Teen drivers and new drivers benefit especially, since their premiums are already elevated and a single at-fault mark has outsized impact on their rate.

For fleet operators and commercial drivers, the ROI math is even stronger. A single commercial vehicle claim can run into tens of thousands of dollars. The dash cam pays for itself on day one of a claim that goes the right way.

I’d put it simply: a dash cam is one of the few car accessories that genuinely pays for itself — not by doing something impressive, but by doing one reliable thing every single day.

Frequently Asked Questions

How much does a dash cam reduce insurance in the UK?

UK drivers can save between 5% and 12.5% on car insurance premiums with insurers that offer a formal dash cam discount, such as Swiftcover. Beyond the direct discount, the indirect savings from protecting your no-claims bonus can be significantly larger over multiple years.

Do any US insurance companies offer a dash cam discount?

As of 2024, most major US insurers do not offer a structured dash cam discount on personal auto policies. However, dash cam footage can prevent wrongful at-fault designations in disputed claims, which protects you from the 40–50% surcharge US insurers typically apply after an at-fault accident.

Does a dash cam help if the other driver lies about an accident?

Yes — this is one of the most powerful uses of a dash cam. If another driver provides a false account of an accident, clear footage showing the actual sequence of events gives your insurer and, if needed, a court a definitive record. Without it, disputed claims often result in split liability or a default at-fault ruling against the innocent driver.

What resolution does a dash cam need to be accepted by an insurer?

Most insurers require at least 1080p Full HD resolution to confirm license plates, timestamps, and road markings clearly. Low-resolution footage below this standard is often inconclusive and may not be accepted as reliable evidence in a liability dispute.

Will my dash cam footage void my insurance policy?

Dash cam footage cannot void your policy on its own. However, if footage clearly shows you committed a traffic offense — such as running a red light — your insurer can use that evidence when determining liability. The footage reflects reality; it does not change the legal outcome of what actually happened.

Is a dual-channel dash cam worth the extra cost for insurance purposes?

Yes. Rear-end collisions are the most common accident type, and a rear camera provides evidence that a single front-facing cam cannot. Dual-channel systems cost $30–$80 more than single-channel options and cover the most frequently disputed accident scenarios.

I’m Alex Rahman, a car enthusiast and automotive writer focused on practical solutions, car tools, and real-world driving advice. I share simple and honest content to help everyday drivers make better decisions.