Do I Need to Tell My Insurance I Have a Dash Cam? (The Full Answer)

You are not legally required to tell your insurer you have a dash cam in most countries. But your policy contract may require it if the camera is hardwired. Disclosing it voluntarily can earn you a discount. Failing to mention it rarely voids your policy — but it can complicate a claim.

I installed my first dash cam on a rainy Tuesday after a near-miss on the motorway. The other driver claimed I cut him off. I knew I hadn’t — but I had zero proof. That experience changed how I thought about driving forever.

Then came the question I wasn’t ready for: Do I need to tell my insurer about this?

I’m Alex Rahman, and I’ve spent years helping drivers understand the small print that insurers hope you won’t read. This question trips up thousands of drivers every year — and the answer is more nuanced than a simple yes or no.

Here is what you actually need to know, whether you just bought a Nextbase 622GW or you’ve had a dashcam sitting in your glovebox for two years without saying a word to your insurer.

- No law in the UK, US, or EU requires you to disclose a dash cam to your insurer.

- Your insurance policy contract may require declaration if the dashcam is hardwired into your vehicle’s electrics.

- Many UK insurers — including Admiral and Aviva — offer premium discounts for dashcam owners who declare their device.

- Dash cam footage can help you win a claim — but it can also be used as evidence against you.

- If in doubt, always check your policy’s modification clause and call your insurer directly.

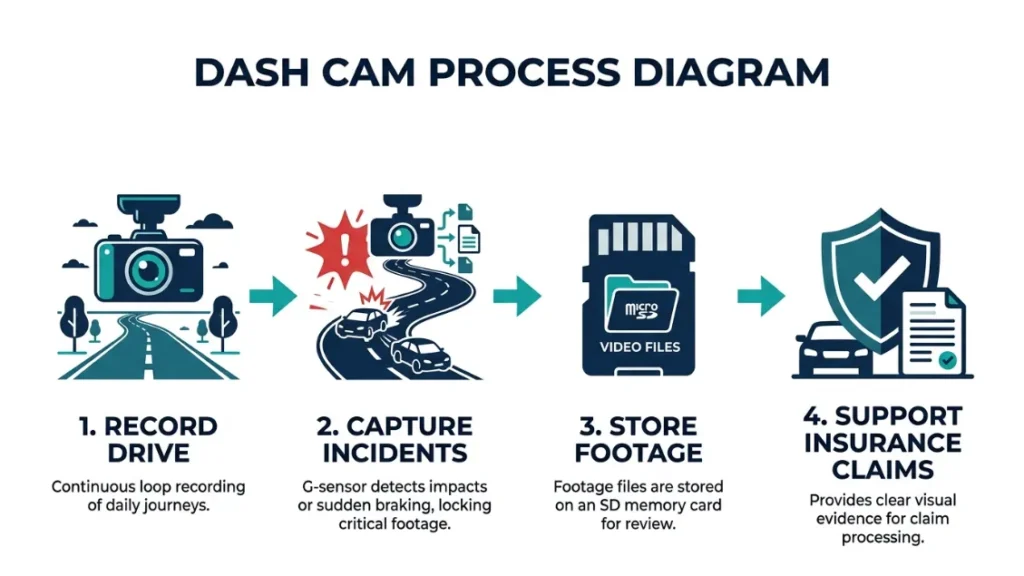

What Is a Dash Cam and Why Does It Matter to Your Insurer?

A dash cam is a small camera mounted to your windscreen or dashboard that records your drive continuously. It stores footage on a loop, capturing accidents, near-misses, and even attempted insurance fraud. In 2023, over 40% of UK drivers owned one — up from just 15% in 2018.

Insurers pay attention to dash cams for two reasons. First, footage can resolve disputed claims quickly. Second, drivers who use dashcams tend to drive more carefully — which means fewer claims. That second point is why some insurers reward you for owning one.

But here is the complication: a dashcam can also be classed as a vehicle modification. And modifications, depending on your policy, sometimes need to be declared.

How Insurers View Dash Cams Differently from Other Modifications

Insurers treat modifications on a spectrum of risk. A sports exhaust raises your risk profile. A tinted windscreen might too. A dash cam, in most cases, does not increase your risk at all — it arguably reduces it.

This is why most insurers do not require you to declare a dash cam as a standard modification. The Association of British Insurers (ABI) confirmed in their 2022 guidance that dashcams are not typically considered risk-altering modifications.

However, hardwired dashcams are a grey area. If your device is permanently wired into your vehicle’s fuse box, some insurers classify that as an electrical modification — and that may trigger a declaration requirement.

Why More Drivers Are Asking This Question in 2024

Dashcam ownership in the UK hit an all-time high in 2023, with brands like Nextbase, Vantrue, and BlackVue leading sales. As more drivers install front and rear cameras, the insurance question becomes more pressing.

At the same time, more insurers are actively advertising dashcam discount schemes. That visibility has made drivers curious — and cautious. Nobody wants to make a claim only to discover their footage complicates things.

Are You Legally Required to Tell Your Insurance About a Dash Cam?

No law in the UK, US, or EU requires drivers to declare a dash cam to their insurance provider. This is a contract question, not a legal one. What matters is what your specific policy document says — not what the law says.

That distinction is important. Many drivers assume there must be some regulation behind this. There isn’t. The obligation, if any exists, comes from your policy terms — specifically the modification or material change clauses.

What the Law Actually Says (UK, US, and EU Compared)

In the United Kingdom, no statute requires dashcam disclosure to insurers. The Road Traffic Act 1988 covers insurance requirements but says nothing about dashcams. Your legal obligation is simply to hold valid insurance — not to report every accessory.

In the United States, insurance rules vary by state. No federal law mandates dashcam disclosure. State-level regulations focus on whether a modification affects vehicle safety or emissions — a dashcam does neither. Check your state’s DMV guidelines if you’re unsure.

In the European Union, the picture is similar. No EU directive requires dashcam disclosure to motor insurers. However, EU drivers face separate obligations under GDPR regarding how they store and share footage — more on that in a later section.

Even if the law doesn’t require it, always check your policy’s modification clause. Some insurers define “modification” more broadly than you’d expect — and a hardwired camera might fall under it.

What Your Policy Contract Says — and Why That Matters More Than Law

Your insurance policy is a contract. If that contract says you must declare all modifications to your vehicle, and your insurer classifies a hardwired dashcam as a modification, you’re contractually obliged to disclose it.

Failing to meet a contractual obligation — even an innocent one — can give an insurer grounds to challenge a claim. Not void your policy outright in most cases, but complicate settlement. That is a risk not worth taking for a two-minute phone call.

Read the section in your policy labelled “modifications,” “changes to your vehicle,” or “material facts.” If dashcams are not mentioned explicitly, call your insurer and ask. Get the answer in writing if you can.

Does a Dash Cam Count as a Vehicle Modification for Insurance?

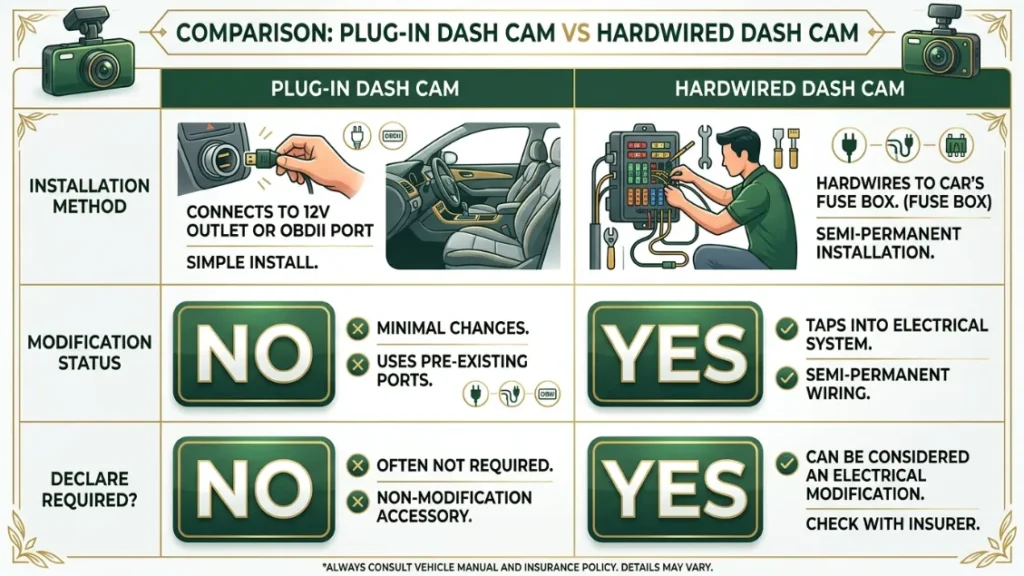

In most cases, a dashcam does not count as a material modification for insurance purposes. Suction-cup mounted cameras that plug into a 12V socket are almost never classed as modifications. Hardwired dashcams sit in a greyer area and may need declaring depending on your insurer’s definition.

The key word is “material.” A material modification is one that changes the vehicle’s performance, value, or risk profile. A dashcam does none of those things in a negative sense — which is why most insurers treat it differently from a turbo upgrade or lowered suspension.

The Definition of a Material Modification and Where Dashcams Fit

A material modification is any change to your vehicle that a reasonable insurer would want to know about before setting your premium. The test is simple: does this change your risk? For dashcams, the answer is no — or even the opposite.

Studies by the road safety charity Road Safety Foundation suggest that dashcam users have fewer at-fault accidents. Some UK insurers cite internal data showing claims are resolved 30–40% faster when dashcam footage is available. That’s a risk reducer, not a risk increaser.

Hardwired Dash Cams vs. Plug-In Models — Which Needs Declaring?

| Type | Installation Method | Likely Modification Status | Declare to Insurer? |

|---|---|---|---|

| Plug-in dashcam | 12V socket or USB | Not a modification | Usually no |

| Hardwired dashcam | Wired into fuse box | Grey area — varies by insurer | Check your policy |

| Integrated OEM camera | Factory-fitted | Not a modification | No |

Can Telling Your Insurer About a Dash Cam Lower Your Premium?

Yes — telling your insurer you have a dashcam can lower your premium, but only if your insurer runs a dashcam discount scheme. Not every insurer does. Those that do typically offer between 5% and 12.5% off your annual premium, which on an average UK policy worth £627 (2024 figures) saves you between £31 and £78 per year.

The logic is simple. Dashcam owners file fewer disputed claims. Fraudulent claims — like staged accidents — are easier to reject when footage exists. That saves the insurer money, and some pass the savings on to you.

Which UK Insurers Offer Dash Cam Discounts Right Now

Admiral offers a dashcam discount scheme where drivers can upload footage for claim verification and receive reduced excess costs. Aviva has integrated dashcam-compatible telematics policies for younger drivers. Direct Line and Churchill offer case-by-case consideration but not a standard discount.

Specialist insurers like Dashcam Insurance (a UK-based broker) exist specifically to match dashcam owners with insurers who value footage. For US drivers, the Insurance Information Institute recommends asking your insurer directly — there is no nationwide standard.

When calling your insurer, say exactly this: “I’ve installed a dashcam. Do you offer any discount for dashcam users, and does it need to be declared?” That one question gets you everything you need in 60 seconds.

How Much Could You Actually Save?

The savings vary more by insurer than by driver profile. Admiral’s dashcam scheme has been reported to reduce excess charges by up to £250 on a successful claim. Aviva’s telematics policies for young drivers can cut premiums by 10–25% when dashcam data is included.

Over five years of driving, a consistent 10% dashcam discount could save you £300–£500 in premium costs alone — not counting the claims advantage. That pays for most mid-range dashcams within the first year.

Discounts exist but aren’t universal. UK drivers have the most options right now. The best approach: tell your insurer, ask for the discount, and get confirmation in writing. It costs nothing to ask and could save you money immediately.

Should You Tell Your Insurer Even If You Don’t Have To?

Yes — in most cases, you should tell your insurer about your dashcam even when it’s not required. The upside is real (discounts, smoother claims). The downside is nearly zero if your device is a plug-in model. For hardwired cameras, disclosing protects you from any contractual challenge later.

This is the decision most articles leave to you without guidance. I’ll give you a direct answer: disclose it. The only exception is if your footage could work against you — and even then, the footage exists whether you declare the camera or not.

The Case For Disclosing Your Dash Cam

Disclosure gives you three advantages. First, you become eligible for any discount your insurer offers. Second, if you make a claim and footage is relevant, your insurer already knows it exists — there’s no surprise, no complication. Third, if your camera is hardwired and your insurer later treats that as an undeclared modification, you’re protected because you told them.

The process takes five minutes. A quick call or online policy update is all it takes. Most insurers log the declaration and that’s the end of it. No premium increase for a plug-in dashcam. None.

The One Risk You Need to Know Before You Decide

Your insurer can request dashcam footage during a claim investigation — even if the footage doesn’t support your version of events. If you declare you own a dashcam and then claim footage was lost or corrupted, that can raise red flags. Never delete or claim to lose footage that exists.

Your dashcam footage belongs to you. But once an insurer knows it exists, they may request it as part of a claim. If the footage is genuinely unavailable due to a technical failure, document that clearly. SD card corruption and overwriting are common — just be honest about what happened.

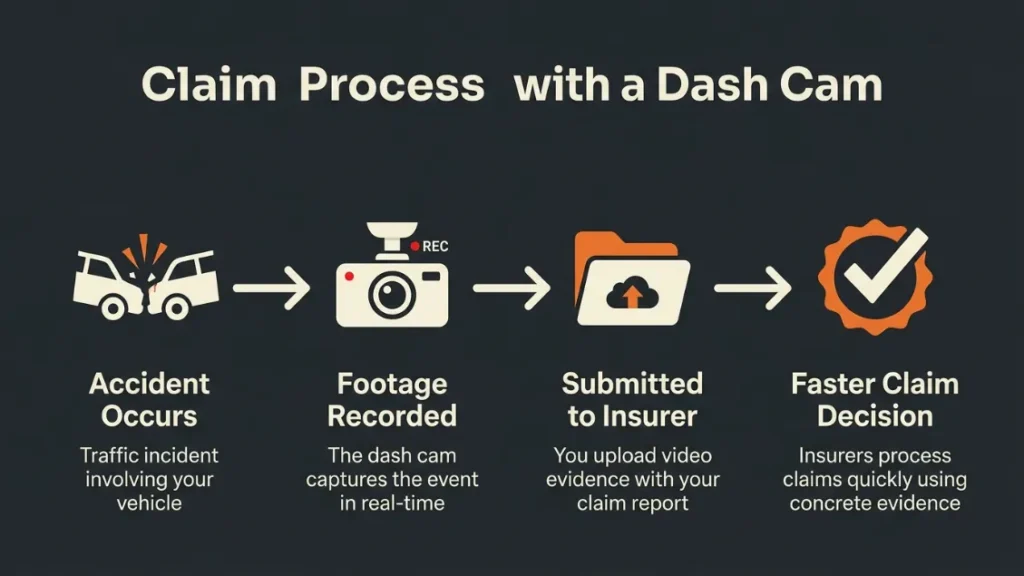

How Does Dash Cam Footage Affect an Insurance Claim?

Dashcam footage can significantly speed up insurance claims and improve their outcome. In the UK, the Motor Insurers’ Bureau reports that dashcam evidence resolves liability disputes in a fraction of the time taken without footage. For drivers who are not at fault, footage is a powerful tool.

But footage cuts both ways. It shows exactly what happened — including your speed, lane position, and reaction time. If those factors are relevant to the claim, your insurer — or the other party’s insurer — will look at them closely.

When Footage Helps Your Claim Get Paid Faster

Footage helps most in three situations: rear-end collisions (proving you were stationary), junction disputes (proving right of way), and insurance fraud attempts like “crash for cash” staged accidents. In all three, clear footage often ends the dispute before it starts.

Insurers love good footage. It removes ambiguity, cuts investigation time, and lets them close files quickly. A claim that might take months to settle can resolve in days with a clear front-facing video showing what actually happened.

Can Your Insurer Use Your Own Footage Against You?

Yes. If you were speeding, distracted, or driving carelessly, your dashcam records that too. An insurer — or the opposing party’s legal team — can request footage and use it to establish your liability. This isn’t unique to dashcams; witness accounts and other camera systems do the same thing.

The answer isn’t to avoid dashcams. It’s to drive the way you’d be happy to prove in a courtroom. That’s good advice regardless of whether a camera is rolling.

Think of your dashcam like a silent witness. It tells the truth — the full truth — without editing or bias. That’s exactly what you want if you’re driving well. And exactly what you don’t want if you’re not.

What About Privacy Laws and Dash Cam Footage?

In the UK and EU, GDPR applies to dashcam footage if it captures identifiable individuals in public. The Information Commissioner’s Office (ICO) in the UK has confirmed that personal dashcam use is covered under a domestic use exemption — meaning you are not classed as a data controller for your own recordings. But this changes the moment you upload or share footage publicly.

Sharing footage on social media, even to document dangerous driving, carries data protection risk if individuals are identifiable. Submitting footage to police as evidence is exempt from GDPR. Sharing with your insurer as part of a claim is also typically covered under legitimate interest.

GDPR and Dashcams — What UK and EU Drivers Must Know

UK drivers submitting footage to their insurer do not need special GDPR permission to do so. The ICO guidance published in 2021 confirms that sharing footage with a third party (like an insurer or the police) for a legitimate purpose — such as resolving a claim — falls within the domestic use exemption.

Business drivers and fleet operators face stricter rules. If a company installs dashcams in commercial vehicles, GDPR compliance is mandatory. That includes data retention policies, driver notification, and secure storage. Fleet managers should consult the ICO’s official guidance before deploying cameras across a fleet.

If you run a small business and use a dashcam in a van or company car, you may be subject to full GDPR obligations — not the domestic use exemption. Drivers must be informed their journeys are recorded, and data must be stored securely and deleted after a defined period.

How to Tell Your Insurance Company About Your Dash Cam

Telling your insurer about your dashcam takes under five minutes and requires no paperwork in most cases. Here is the fastest way to do it correctly.

- Locate your policy documents and find the “modifications” or “changes to your vehicle” section.

- Check whether dashcams are mentioned. If yes, follow those instructions. If no, proceed to step 3.

- Call your insurer’s customer service line or use their online chat or portal.

- Say: “I’ve installed a dashcam. I’d like to declare it and check whether I qualify for a discount.”

- Ask them to confirm in writing (email or portal message) that it’s been logged on your policy.

- Ask specifically: “Will this affect my premium?” — in most cases for plug-in devices, the answer is no.

Keep a record of the conversation. If you use online chat, screenshot the confirmation. That record protects you if questions ever arise during a claim.

Conclusion

Here is the short version: you almost certainly do not need to tell your insurer you have a dashcam by law. But doing so is almost always the smarter move.

If your camera is plug-in, declaring it costs nothing and may save you money. If it’s hardwired, declaring it removes any contractual risk. And in either case, it means your insurer knows a footage record exists — which is exactly the kind of evidence that makes claims go your way.

I’m Alex Rahman, and the one thing I’ve learned from years of reading insurance small print is this: the five-minute phone call you avoid today often costs you hours of stress after an accident. Make the call. Ask the question. And drive knowing your dashcam is working for you, not against you.

Frequently Asked Questions

Do I legally have to tell my insurance company about a dashcam?

No. There is no law in the UK, US, or EU that requires you to declare a dashcam to your insurer. The obligation, if any exists, comes from your policy contract — specifically the modification clause. Always read your policy or call your insurer to confirm.

Will adding a dashcam increase my insurance premium?

In most cases, no. Dashcams are not considered risk-increasing modifications by most insurers. In fact, many UK insurers offer discounts for dashcam owners. A plug-in dashcam is extremely unlikely to raise your premium when declared.

Can my insurance company ask for dashcam footage after an accident?

Yes. If your insurer knows you have a dashcam, they may request the footage as part of their claims investigation. You are generally obliged to cooperate. If footage is lost due to technical failure, document that clearly and report it promptly.

Does a hardwired dashcam need to be declared to my insurer?

It depends on your insurer’s definition of a modification. Hardwired cameras connect to your vehicle’s electrics, which some insurers classify as an electrical modification. Check your policy’s modification clause and call your insurer if you’re unsure — it takes five minutes and removes all risk.

Which insurers offer dashcam discounts in the UK?

Admiral, Aviva, and several specialist brokers offer dashcam-related discounts or reduced excess schemes. Discounts typically range from 5% to 12.5% off annual premiums. The best approach is to call your current insurer and ask directly whether they have a dashcam scheme.

Is dashcam footage covered by GDPR in the UK?

Personal dashcam use falls under a domestic exemption under GDPR, meaning private drivers are not classed as data controllers for their own recordings. Sharing footage with an insurer or police for a legitimate claim is generally permitted. Business and fleet use requires full GDPR compliance, including driver notification and data retention policies.

I’m Alex Rahman, a car enthusiast and automotive writer focused on practical solutions, car tools, and real-world driving advice. I share simple and honest content to help everyday drivers make better decisions.