Does Installing a Dashcam Affect Your Car Insurance (and Can It Save You Money)?

Yes, installing a dashcam can affect your car insurance — usually for the better. Some insurers offer premium discounts of 10–12.5% for dashcam owners. It can also speed up claims and protect you from fraud. Always notify your insurer after fitting one.

A few years back, I was rear-ended at a roundabout. No witnesses. The other driver blamed me. Without proof, my insurer had little to work with — and the claim dragged on for weeks.

I’m Alex Rahman, and that experience pushed me to research everything about dashcams and insurance. What I found surprised me.

A dashcam doesn’t just record your drive. It can lower your premium, protect you after an accident, and even stop fraud before it starts. But there are also risks most articles never mention — like what happens if your own footage works against you.

This guide covers all of it. By the end, you’ll know exactly whether a dashcam is worth fitting — and how to make the most of it if you do.

- Some insurers offer dashcam discounts of up to 12.5% on your annual premium.

- You must notify your insurer when you install a dashcam — failing to do so can cause claim complications.

- Dashcam footage can help resolve claims faster and protect you from staged accident fraud.

- Your own dashcam footage can be used against you if it shows you were at fault.

- A dual-channel dashcam (front and rear) gives you stronger protection than a front-only device.

What Is a Dashcam and Why Do Insurers Pay Attention to It?

A dashcam is a compact video camera mounted on your windshield or dashboard. It records continuously while you drive, saving footage in loops to a memory card. Many models also capture audio, GPS location, speed, and G-force data from impacts.

Insurers pay attention because dashcam footage replaces guesswork with evidence. Road accidents often come down to one driver’s word against another’s. A clear video recording changes that dynamic completely.

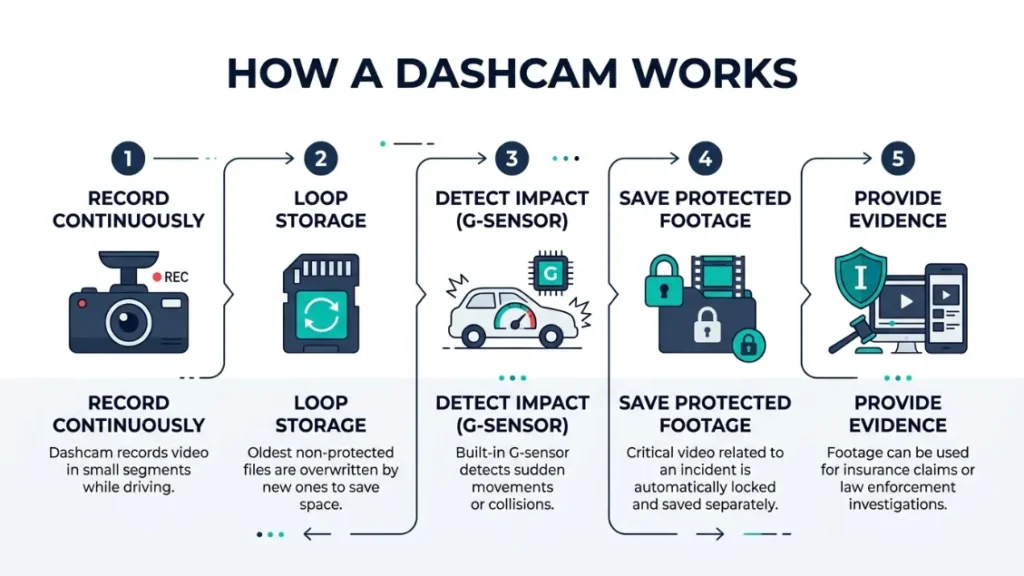

How Does a Dashcam Record and Store Footage?

Most dashcams use loop recording. When the memory card fills up, the camera overwrites the oldest footage automatically. If a collision happens, a built-in G-sensor detects the impact and locks that clip so it doesn’t get erased.

Higher-end models like the Nextbase 622GW — a UK-favourite trusted by millions of drivers — also offer parking mode. This keeps recording even when the engine is off, protecting against hit-and-run incidents in car parks.

The footage is stored locally on the device. Some newer cameras offer cloud backup, which gives you an off-device copy that no one can tamper with or remove after an incident.

Why Insurance Companies Care Whether You Have One

Insurers spend billions settling disputed claims every year. In the UK alone, the Association of British Insurers (ABI) estimates that fraudulent claims cost the industry over £1 billion annually — costs that get passed on to honest drivers through higher premiums.

A dashcam cuts through dispute and fraud. It helps insurers close claims faster, fight fraudulent cases, and identify the at-fault driver accurately. That saves them money — and gives them a reason to reward you for having one.

Choose a dashcam with a wide-angle lens (140 degrees or more) and at least 1080p resolution. Insurers need to clearly read number plates and road signs from your footage to accept it as evidence.

Does a Dashcam Actually Lower Your Car Insurance Premium?

The direct answer is: it depends on your insurer. Not every provider offers a dashcam discount, but a growing number do — and the savings can be meaningful over a full policy year.

The insurance industry is slowly catching up with dashcam technology. As more providers see the claim-cost benefits of video evidence, discount programs are becoming more common — especially in the UK and parts of Europe.

Which Insurance Providers Offer a Dashcam Discount?

In the UK, several mainstream insurers actively reward dashcam ownership. Admiral Insurance and AXA are among providers that have acknowledged dashcam discounts in their policy discussions. Specialist providers like Dash Cam Insurance and Smartwitness have built dashcam evidence directly into their claims processes.

In the US, the dashcam discount market is less structured. Most major insurers — including State Farm, Geico, and Progressive — do not advertise a direct dashcam discount. However, some usage-based programs reward safe driving behaviour, which a dashcam can support indirectly.

Always call your insurer directly and ask. The question to use: “Do you offer a discount or any policy benefit for drivers who install a dashcam?” You may be surprised at the answer.

How Much Can You Realistically Save with a Dashcam?

UK drivers with dashcam-friendly insurers have reported savings of 10% to 12.5% on their annual premium. On a £600 policy, that’s £60–£75 back in your pocket each year.

A quality dashcam like the Garmin Dash Cam 57 costs around £100–£130. At a £70 annual saving, the device pays for itself in under two years — and then keeps saving you money every year after.

| Annual Premium | 10% Discount Saving | 12.5% Discount Saving | Dashcam Break-Even Point |

|---|---|---|---|

| £400 | £40/year | £50/year | ~2.5 years |

| £600 | £60/year | £75/year | ~1.5 years |

| £900 | £90/year | £112.50/year | ~1 year |

Do You Need to Tell Your Insurer You Have a Dashcam — And What Happens If You Don’t?

Yes — you should always notify your insurer when you install a dashcam. Most insurers don’t require it as a strict policy condition, but telling them opens the door to discounts and prevents any complications if footage becomes relevant in a claim.

Here’s the practical reality. If you’re involved in an accident and submit dashcam footage, your insurer will know you had a device installed. If you never disclosed it, some insurers may question the timeline. That’s a headache you don’t need during a stressful claim.

More importantly, some policies do list modifications to your vehicle in the disclosure requirements. A hardwired dashcam — one connected directly to your car’s fuse box — could technically count as a vehicle modification. Always check your policy wording.

Never assume a dashcam is automatically covered by your car insurance if it’s stolen. Most standard car policies don’t cover in-car electronics. Check whether your home contents insurance or a specialist gadget policy covers your dashcam separately.

How Dashcam Footage Speeds Up Insurance Claims and Protects You After an Accident

Dashcam footage is one of the most powerful tools you can hand to your insurer after a collision. It replaces weeks of back-and-forth with a clear, timestamped record of exactly what happened — cutting claim settlement time dramatically.

When both drivers dispute fault, insurers must investigate. Without evidence, that process can take months. Video footage often resolves the dispute in days.

What Happens When You Submit Dashcam Footage to Your Insurer?

After an accident, contact your insurer as soon as possible. Tell them you have dashcam footage. They’ll usually ask you to upload it through their portal or send it digitally. Keep the original file — never send your only copy.

Your insurer reviews the footage alongside the police report, witness statements, and any other evidence. If your footage clearly shows you weren’t at fault, your insurer can pursue the other party’s insurance for full recovery — a legal process called subrogation.

This protects your no-claims discount. Without footage proving the other driver’s fault, your insurer might settle under your own policy — which can affect your discount even when you weren’t responsible.

How Dashcams Stop Crash-for-Cash Fraud in Its Tracks

Crash-for-cash fraud is a serious organised crime. Fraudsters deliberately cause accidents — often by braking suddenly in front of innocent drivers — then claim whiplash and vehicle damage. The Insurance Fraud Bureau (IFB) estimates this type of fraud costs UK drivers around £340 million per year.

A dashcam is one of the most effective deterrents available. Fraudsters actively avoid vehicles with visible dashcams because video evidence immediately destroys their false claim.

If you are targeted despite having a dashcam, your footage will show the deliberate braking pattern, road conditions, and your following distance — giving your insurer and the police exactly what they need to act.

After any incident — even a minor one — immediately remove and secure your memory card. Back up the footage to a computer or cloud storage before doing anything else. Footage can be overwritten if the camera keeps running after the event.

Can Your Dashcam Footage Be Used Against You in a Claim?

Yes — and this is the part most dashcam guides skip. If your footage shows you were speeding, driving too close, or distracted before a collision, that evidence can work against you in a claim or even in a legal case.

Your insurer has a duty to settle claims based on the facts. If your own footage reveals you were at fault, they’ll use it — because not using it would be bad faith on their part.

In some jurisdictions, dashcam footage submitted during a claim becomes part of the legal record. Prosecutors and civil courts can access it. Driving within the law at all times is your best protection — and that’s ultimately the point of having the device.

Think of your dashcam as a silent, impartial witness. It records everything without bias. If you drive responsibly, it will always be on your side. If you don’t, it won’t protect you from the truth.

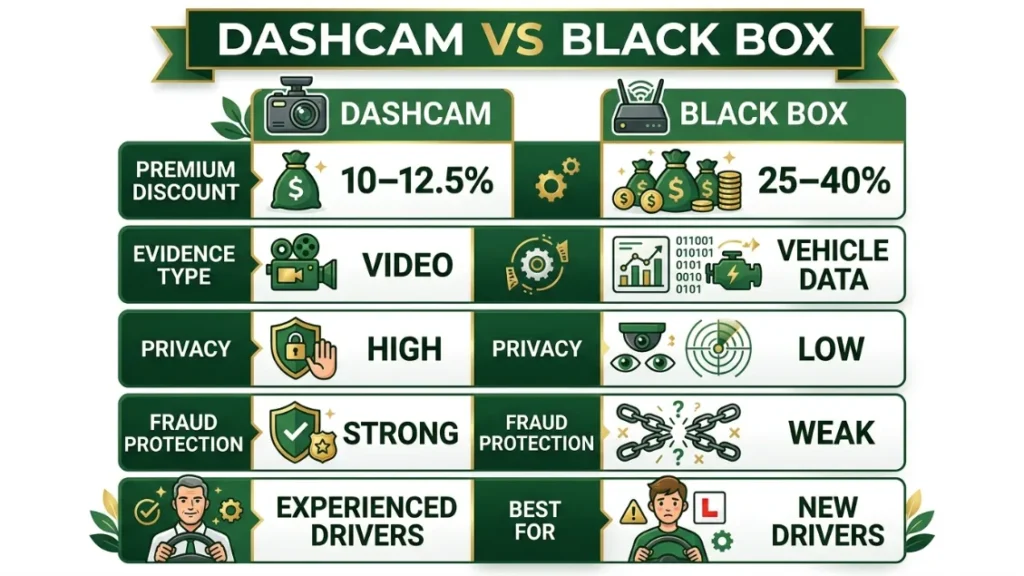

Dashcam vs Black Box — Which One Helps Your Insurance More?

Both dashcams and black boxes (telematics devices) can lower your insurance costs — but they work in very different ways. Understanding the difference helps you choose the right tool for your situation.

A black box monitors your driving behaviour continuously — speed, braking, cornering, and time of day. Insurers use this data to price your policy based on how safely you actually drive. It’s especially effective for young or new drivers who lack a no-claims history.

A dashcam records video evidence. It doesn’t report your driving to your insurer in real time — but it protects you when accidents happen and can qualify you for a one-time premium discount.

| Feature | Dashcam | Black Box / Telematics |

|---|---|---|

| Premium discount | Up to 12.5% (one-time) | Up to 25–40% (behaviour-based) |

| Claim evidence | Strong — video footage | Moderate — data logs |

| Privacy | High — footage stays local | Low — insurer monitors live |

| Fraud protection | Excellent | Weak |

| Best suited for | Experienced drivers | Young / new drivers |

Some drivers use both. A black box manages their premium based on driving behaviour, while a dashcam provides video protection in disputes. If your insurer supports both, it’s worth exploring.

Does the Type of Dashcam You Install Make a Difference to Insurers?

Yes — the type, quality, and installation method of your dashcam all influence how useful it is for insurance purposes. Not all cameras are equal in the eyes of your insurer.

Front-Only vs Dual-Channel Dashcams — Which Do Insurers Prefer?

A front-only dashcam records what happens ahead of you. That covers most common collision scenarios — rear-end crashes, junction accidents, and road rage incidents caught on camera.

A dual-channel dashcam adds a rear-facing camera. This gives you footage of tailgating, rear-end impacts, and any incidents behind the vehicle. For insurance purposes, a dual-channel setup is significantly more useful — especially if you’re hit from behind, which is one of the most disputed accident types.

Models like the Vantrue N4 go further with a three-channel setup: front, interior, and rear. This is particularly valuable for rideshare drivers or fleet operators where what happens inside the vehicle also matters.

Does a Hardwired Dashcam Affect Your Insurance Differently?

A hardwired dashcam connects directly to your car’s fuse box. This powers parking mode — recording even when the engine is off. For insurance, parking mode evidence is extremely valuable for hit-and-run claims in car parks, where you have no witness and no dashcam trigger event to rely on.

The trade-off: hardwiring is a vehicle modification. Some insurers classify it as such, which means you must disclose it. A professional installation by a certified auto electrician also protects your vehicle warranty, which some insurers factor into policy eligibility.

In the UK, if a dashcam records other people — pedestrians, other drivers — on public roads, GDPR rules apply. You can record legally for personal use and insurance claims. But sharing footage publicly on social media without consent can create legal risk. Always check ICO guidance before posting dashcam videos online.

Step-by-Step: How to Tell Your Insurer About Your Dashcam and Maximize Your Discount

Notifying your insurer about your dashcam takes five minutes and could save you money immediately. Here’s exactly how to do it.

- Install your dashcam and test that it records clearly — check footage quality before contacting anyone.

- Find your insurer’s customer service number or online portal — it’s on your policy documents or their website.

- Tell them you’ve installed a dashcam and ask specifically: “Do you offer a premium discount or any policy benefit for dashcam owners?”

- If they say yes — ask what proof they need (receipt, model name, or installation evidence).

- Note the name of the agent you spoke to and the date — keep a written record of the conversation.

- Ask your insurer to confirm any discount or policy update in writing — email or letter.

- At renewal, re-confirm your dashcam is still registered and that the discount still applies.

Notify your insurer immediately after installation. Ask directly about discounts. Get any benefit confirmed in writing. Repeat the check at every renewal — discounts can change between policy years.

Is Installing a Dashcam Worth It for Insurance Purposes? (Honest Verdict)

For most drivers — yes, a dashcam is worth installing. The financial case is solid for anyone with an insurer that offers a discount, and the protection benefit exists for everyone regardless of discounts.

Here’s my honest breakdown after years of researching this topic:

- If your insurer offers a discount: The dashcam pays for itself within 1–2 years and then saves you money indefinitely.

- If your insurer offers no discount: The protection value alone — faster claims, fraud deterrence, no-claims preservation — still makes it worthwhile for most drivers.

- If you drive in high-fraud-risk areas: A dashcam is close to essential. Crash-for-cash fraud clusters in specific urban areas, and a visible camera is your strongest deterrent.

- If you’re a new or young driver: Consider combining a dashcam with a black box policy for maximum savings and maximum protection.

The one scenario where a dashcam adds less value: if you rarely drive, have a perfect claims history, and your insurer offers zero discount. Even then, parking mode on a hardwired camera protects your parked vehicle in a way nothing else can.

A dashcam won’t make bad driving cheaper. But it will make responsible driving safer, faster to prove, and — with the right insurer — noticeably less expensive.

Frequently Asked Questions

Does a dashcam lower your car insurance premium?

It can. Some UK insurers offer discounts of 10–12.5% for dashcam owners. Not all providers do, so call your insurer directly and ask whether they offer any premium benefit for having a dashcam fitted.

Do I need to tell my insurer I have a dashcam?

Yes — always notify your insurer when you install one. It’s the best way to access any available discount and avoid complications if footage becomes relevant during a claim. A hardwired dashcam may also count as a vehicle modification under some policies.

Can dashcam footage be used against me in an insurance claim?

Yes. If your footage shows you were speeding, following too closely, or distracted, your insurer and potentially the courts can use it as evidence against you. Your dashcam records everything impartially — including your own driving.

Which type of dashcam is best for insurance purposes?

A dual-channel dashcam — recording both front and rear — gives you the strongest insurance protection. It captures rear-end impacts, which are among the most disputed accident types. Choose a model with at least 1080p resolution and a wide-angle lens for clear number plate footage.

Does a dashcam protect your no-claims discount?

It can, significantly. If your footage proves another driver was at fault, your insurer can recover costs through subrogation — meaning your no-claims discount stays intact. Without footage, disputed claims often settle in ways that affect your discount even when you weren’t responsible.

Is a dashcam better than a black box for saving money on insurance?

They work differently. A black box adjusts your premium based on ongoing driving behaviour and can save more over time — especially for young drivers. A dashcam gives a smaller one-time discount but provides stronger claims protection and fraud deterrence. Many drivers benefit from using both.

I’m Alex Rahman, a car enthusiast and automotive writer focused on practical solutions, car tools, and real-world driving advice. I share simple and honest content to help everyday drivers make better decisions.